Closing Entries in Accounting: Everything You Need to Know +How to Post Them

From the Deskera “Financial Year Closing” tab, you can easily choose the duration of your accounting closing period and the type of permanent account you’ll be closing your books to. Now, the income summary account has a zero balance, whereas net income for the year ended appears as an increase (or credit) of $14,750. Now that we know the basics of closing entries, in theory, let’s go over the step-by-step process of the entire closing procedure through a practical business example. That’s exactly what we will be answering in this guide – along with the basics of properly creating closing entries for your small business accounting. And so, the amounts in one accounting period should be closed so that they won’t get mixed with those in the next period. For partnerships, each partners’ capital account will be credited based on the agreement of the partnership (for example, 50% to Partner A, 30% to B, and 20% to C).

Explore our full suite of Finance Automation capabilities

The Income Summary balance is ultimately closed to the capital account. Implementing these best practices helps streamline the month-end close process, making it more efficient and accurate. This allows your business to focus on strategic goals and decision-making with confidence. You don’t have to build processes from scratch — instead, start with templates whenever applicable.

- All expenses can be closed out by crediting the expense accounts and debiting the income summary.

- Therefore, we can calculate either profit margin for this company or how much it lost over the year.

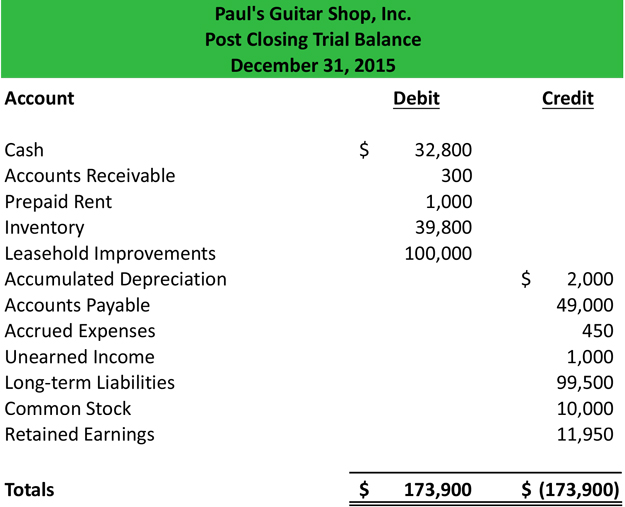

- This givesyou the balance to compare to the income statement, and allows youto double check that all income statement accounts are closed andhave correct amounts.

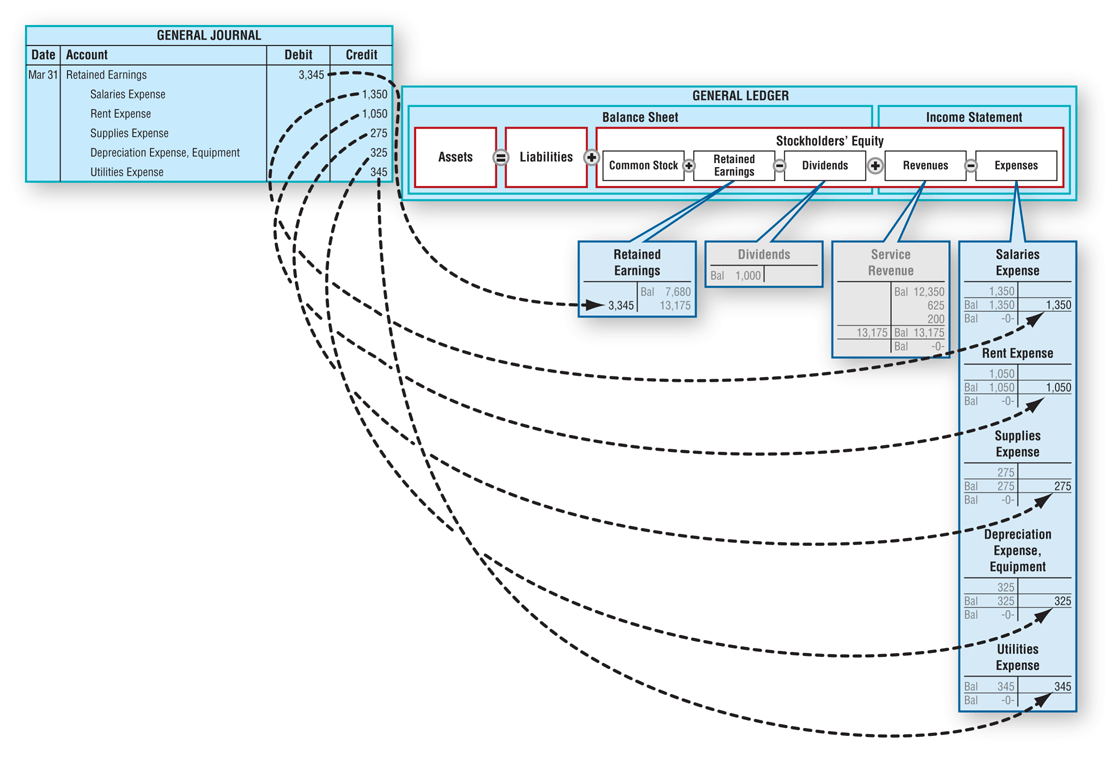

- Now, all the temporary accounts have their respective figures allocated, showcasing the revenue the bakery has generated, the expenses it has incurred, and the dividends declared throughout the past year.

Step 3 – Close Income Summary to Retained Earnings

For the past 52 years, Harold Averkamp (CPA, MBA) hasworked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. He is the sole author of all the materials on AccountingCoach.com. For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. Someone on our team will connect you with a financial professional in our network holding the correct designation and expertise. Our writing and editorial staff are a team of experts holding advanced financial designations and have written for most major financial media publications.

What are Temporary and Permanent Accounts?

Then, credit the income summary account with the total revenue amount from all revenue accounts. This process ensures that your temporary accounts are properly closed out sequentially, and the relevant balances are transferred to the income summary and ultimately to the retained earnings account. Since dividend and withdrawal accounts are not income statement accounts, they do not typically use the income summary account. These accounts are closed directly to retained earnings by recording a credit to the dividend account and a debit to retained earnings. If you paid out dividends during the accounting period, you must close your dividend account.

Both closing and opening entries record transactions, but there is a slight variation in their purpose. Permanent accounts, also known as real accounts, do not require closing entries. Examples are cash, accounts receivable, accounts payable, and retained earnings.

Permanent versus Temporary Accounts

Now that the income summary account is closed, you can close your dividend account directly with your retained earnings account. You need to use closing entries to reduce the value of your temporary accounts to zero. That way, your next accounting period does not have a balance in your revenue or expense account from the previous period. Then you are going to create a journal entry to transfer the balance of each temporary account to the appropriate permanent account.

Permanent accounts track activities that extend beyond the current accounting period. They’re housed on the balance sheet, a section of financial statements that gives investors an indication of a company’s value including its assets and liabilities. Once all of the temporary accounts have been closed, review the journal entries to ensure that they are accurate and complete.

The total debit to income summary should match total expenses from the income statement. In summary, permanent accounts hold balances that persist from one period to another. In contrast, temporary accounts capture transactions and activities for a specific period and require resetting to zero with closing entries. Closing entries are journal entries made at the end of an accounting period, that transfer temporary account balances into a permanent account.

Take, for example, three common accounting procedures — revenue recognition, fixed asset depreciation, and software capitalization. In the most ideal close, teams would accomplish all of these tasks but that’s rarely the case. Similarly, vendor invoice definition and meaning while textbooks might say that teams should account for every single transaction in a month, that’s also far from reality. When you manage your accounting books by hand, you are responsible for a lot of nitty-gritty details.

It’s necessary to properly assess depreciation for items like fixed assets and to amortize capitalized expenses as they each affect your balance sheet and taxable income. All modern accounting software automatically generates closing entries, so these entries are no longer required of the accountant; it is usually not even apparent that these entries are being made. The month-end close is when a business collects financial accounting information. Using the above steps, let’s go through an example of what the closing entry process may look like. Adjusting entries are used to modify accounts so that they’re in compliance with the accrual concept of recording income and expenses.